State-Owned Enterprises and Economic Development in Asia

Next, we evaluate the contribution of SOEs by examining their equity. Total equity is the difference between a corporation’s assets and its tenabilities.[vii] Figure 1.2 breaks down by sector the total equity value of the countries in 2010–2018. Distribution of equity depicts a dominance of SOEs in the primary sectors (agriculture and mining); manufacturing; and electricity, gas, and water supply. Collectively, these three sectors comprised about 70% of the SOEs’ total equity value. In other sectors during 2010–2018, construction, trade and transport, information and communication, and financial and insurance activities contribute 10.3%, 6.4%, 4.6%, and 4.7% of total equity value, respectively.

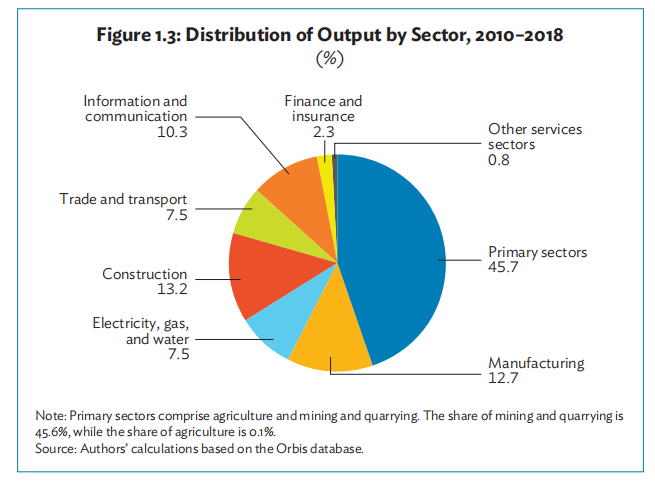

Next, we measure sectoral distribution of output through gross value added. Figure 1.3 shows that during 2010–2018, the primary sector alone accounts for 45.7% of total output. Similarly, the manufacturing; construction; electricity, gas, and water; and information and communication sectors’ contribution to total output during 2010–2018 is estimated to be 12.7%, 13.2%, 7.5%, and 10.3%, respectively. Overall, the contribution of the services sector to SOE output remained around 21%.

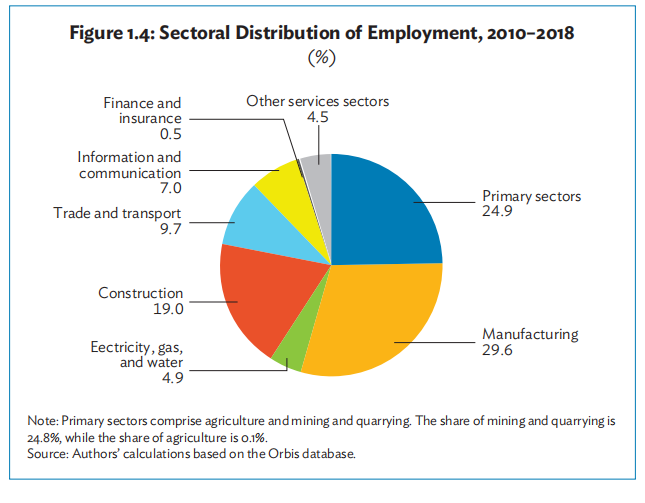

In most of the selected developing member countries (DMCs) in our study, SOEs also provide employment opportunities to the labor force. The sectoral distribution of SOE employment shows that the manufacturing sector absorbs 30% of the labor force, followed by primary sectors which employ about 25% of workers. The construction, information and communication, trade and transport, and energy and water sectors also contribute a significant share in employment (Figure 1.4).

1.5 SOEs’ Financial Performance and Objectives

In analyzing the various measures of efficiency and profitability of public enterprises, it is important to interpret SOE financial performance data with great caution. SOEs typically have public service obligations imposed on them, such as price suppression, servicing uneconomic markets, and various employment-related restrictions. They may not have full commercial freedom in their managerial appointments, capital acquisitions, and product mixes. More broadly, the government may regard them as “agents of development,” which entails additional noncommercial obligations.

Viewed in this context, most public enterprises are not expected to be financially profitable since they provide crucial public goods and are engaged in promoting regional development. For example, the provision of public services in remote areas might not be as financially profitable as in urban areas; nevertheless, such services are equally important for inclusive and sustained development.

In many cases the financial analysis of SOEs is practically meaningless, because of the plethora of explicit and implicit subsidies and obligations affecting their operations (Box 1.1). Unlike private enterprises, the government provides various types of subsidy and capital injections to SOEs when their sources of revenue fall short of covering costs or when they are avoiding default. The subsidies may include privileged market power (i.e., restrictions on barriers to entry and other anticompetitive provisions), state-supported or guaranteed access to preferential finance, and sales/contract guarantees. These subsidies may be so large as to crowd out productive private sector investment, as appears to be the case in Viet Nam. Given these various considerations, on net, the profitability and efficiency of SOEs tend to be generally lower than their private counterparts.