State-Owned Enterprises and Economic Development in Asia

Introducing international best practices, such as transparency, proper accounting, and realistic balance sheets,[viii] can be particularly helpful in improving the quality and worth of public assets. Recent research by the International Monetary Fund (IMF) (2018) comprising 31 countries and covering 61% of the global economy suggests that with proper management, even a higher return of only 1% on public wealth worldwide can add about $750 billion annually to public revenues. Similarly, professional management of public assets such as SOEs among central governments can raise returns by as much as 3.5% and generate an extra $2.7 trillion worldwide. These are substantial gains and are more than the total current global spending on national infrastructure for transport, power, water, and communications combined (Detter and Folster 2015).

Recent episodes of financial crises have exposed many countries to external demand shocks and reemphasized the importance of effective management of public assets and SOEs. The huge size of public wealth across countries and the scars from the global crisis underline the necessity to effectively manage public assets. Further, it is also essential for governments to rebuild their balance sheets by reducing debt and investing in high-quality assets (Detter and Folster 2015). For example, once governments understand the size and nature of public assets and start managing them efficiently, the potential gains could be as high as 3% of GDP a year. These are quite substantial gains and roughly equal to annual corporate tax collections across advanced economies (IMF 2018).

It is, however, important to note that the long-term objective of governments is not merely to maximize the net worth of public assets, but to provide quality goods and services as well. Nevertheless, effective asset management allows governments to raise expenditures during times of crisis and help maintain macroeconomic stability. Viewed in this context, governments that believe their net worth is too low to ensure these objectives may choose to improve the net worth of public assets as one of their operational goals. Empirical evidence corroborates the fact that financial markets consider governments’ asset positions in addition to debt levels when determining borrowing costs.

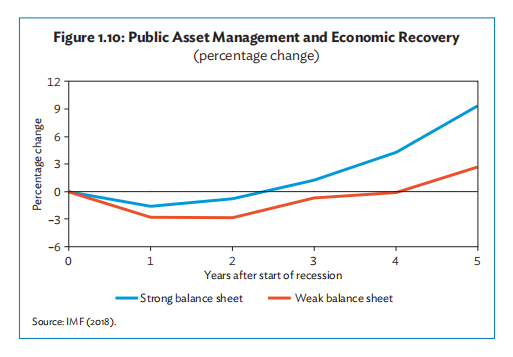

One way to gain insight on the health of the government’s public finance is to examine its public sector balance sheet. As empirical evidence shows (Figure 1.10) countries that have a strong balance sheet and professional management of public assets have had a quick economic recovery (IMF 2018).

Figure 1.10 shows that economies entering a slump with a strong balance sheet and with ample fiscal space are better able to mitigate the impact of the recession and are quick to recover. Economic recovery in these economies started approximately after the second year from the start of the recession. On the contrary, those with a weak balance sheet suffered the adverse impact of the recession on a relatively longer scale and started to recover only four years after the recession began.

This discussion shows that a systematic analysis of the public sector’s balance sheet and that of its assets provides a broader fiscal picture beyond debt and fiscal deficits. As a result, governments and policy makers are in a better position to allocate resources optimally. Effective asset management enables governments to identify risks and take remedial measures in due time rather than deal with the consequences after problems occur. Hence, efficient management of public assets and SOEs not only help improve fiscal position but also quality of public service delivery.

1.10 Reforming and Restructuring SOEs

Early SOE Reforms and Privatization: Evidence from the 1970s and 1980s suggest that, on average, SOEs in many countries have performed poorly compared with private firms, partly because of the difficulty reconciling multiple policy goals. The ensuing heavy financial loss becomes an unsustainable burden on the public budget and banking system. Consequently, various governments since the 1980s have introduced reforms such as exposing SOEs to competition, imposing hard budget constraint, and introducing institutional and managerial changes. As a result, many SOEs were commercialized and eventually corporatized into separate legal entities, and governments developed performance contracts with SOEs to monitor performance and hold managers accountable for results (World Bank Group 2014).

Many developing countries have drafted laws to regulate SOE operations in an effort to improve SOE performance. But without meaningful corporate planning and independent management, many laws and regulations virtually proved to be a pro forma exercise not much relevant to enhancing the performance of public enterprises. In several countries, frequent transfers of managers, directors, and supervisors also diminished the commitment to meet the long-term needs of these enterprises. Even so, SOE managers generally had to face a number of disincentives to adapt to new challenges—especially as many of these companies were insulated from market signals, with their prices controlled, their market protected, and for whom government loans were readily available.

The early reforms introduced by governments across the globe produced some improvements but fell short in implementation. Generally, autonomy in commercial decision-making remained limited, and more importantly, employing financial discipline during a period of hard budget constraint proved difficult without the corresponding restrictions on SOE borrowing from the banking system and from state-owned banks in particular. Implementing performance contracts with SOE management also proved problematic and produced mixed results.

The modest outcome of reforms led many countries to privatize SOEs. During the 1990s and in the early 2000s, financial and nonfinancial SOEs were privatized through various means such as auctions, strategic sales, vouchers, public stock offerings, and management and employee buyouts. The privatization of SOEs was perceived to be a means to eliminate SOE deficits from the national budget, attract private investors with capital and managerial know-how, and achieve efficiency gains through SOE reforms. As a result, the number of SOEs globally declined.

However, privatization was often handled poorly, creating wealth for a few and sometimes leading to high prices for essential goods and services. In developing countries, privatization of SOEs raised concerns and roused sensitivities about foreign ownership of strategic enterprises, and generally proved to be unpopular with the public because of higher infrastructure tariffs and employment losses. As a consequence, widespread privatization stopped around 2000 (World Bank Group 2014).

In the aftermath of the 2007–2008 global financial crisis with capital markets in turmoil, investors’ interests waned and SOE privatization slackened. Governments bailed out failed banks and public enterprises in emerging markets including the PRC, contributing to a dramatic increase in government purchases of corporate equity which had already started in 2008 (Reverditto 2014). Ironically, the crisis itself triggered a new debate on the effective role of government in economic affairs from which emerged a growing interest in public enterprises (World Bank Group 2014).

Modern SOE Reforms: Worth noting also from the viewpoint of improving the performance of public enterprises is that privatization is not the only option. Other intermediate solutions are available as well, such as for example: (i) the government can sell some shares of an SOE and still retain majority control; (ii) the government can retain its whole or majority ownership and contract out management only in certain sectors; or (iii) the government can restructure SOEs and make them more efficient drivers of growth. Indeed, evidence indicates that restructuring is often more important than privatization (Chang 2013). The Philippines’ case study provides invaluable insights about the importance of private sector participation and reforms, which helped transform a loss-making public company into a commercially viable entity (Box 1.2).[ix]

Box 1.2: SOE Reforms – Manila Water

The Metropolitan Waterworks and Sewerage System (MWSS), a state-owned enterprise (SOE) in the Philippines, tells the story of how improving governance and fostering competition have enhanced public service delivery. The MWSS is an interesting example of how the public–private partnership concept can be used to transform a once ailing public company into a commercially viable one.

Before the 1997 reforms, the underperforming MWSS was burdened by large debts. Unable to invest in much-needed water system improvements, it provided poor water quality and intermittent supply. System losses due to poor service and leaks in 1997 amounted to almost 60%, while water coverage was a mere 67%, of which only 26% had 24/7 water supply. In addition, non-revenue water hit almost 60%. The government was unable to increase water tariffs because customers were unwilling to pay for poor service. Furthermore, the MWSS suffered from poor financial performance. Eventually, the Philippines faced a severe water crisis triggered in part by the events that followed El Niño during the 1990s.

Prompted to resolve the crisis, the government selected the concession model to introduce reforms. This led to two separate concession agreements with Maynilad and Manila Water for waterworks rehabilitation, both spanning 25 years. It divided Metro Manila into two areas—east and west. The government assigned Manila Water to be responsible for the east zone and put Maynilad in charge of the west. It introduced reforms and brought in investments in both hard and soft infrastructure and adopted a corporate-style governance, aiming specifically to improve water delivery and wastewater services to existing customers, enhance operating efficiency, and expand service coverage.

As a result of the reforms, water coverage in 2002 increased to 82% for Manila Water and 78% for Maynilad from only 67% before the privatizations. Water availability rose to 21 hours from under 17 hours, and the quality of water improved significantly. The reforms also succeeded in bringing in efficiency gains while reducing operational costs. Likewise, the ratio of staff to 1,000 connections fell from 9.8 to 4.1.

Source: Authors, based on Chia et al. (2007)

In many developing countries, SOEs are generally attached to a sector ministry, with the Ministry of Finance often playing the key role. However, the oversight of sector ministries often appears to be questionable, and combined with rampant interventions, undermines the performance of public companies.

These ministries are responsible for making decisions pertaining to SOE investments and expansion, which directly influence the quality of public service delivery. But, improving the oversight and the caliber of these ministries is a difficult and challenging task. Malaysia is an example of successful SOE restructuring where state investment funds oversee SOEs or government[1]linked companies (GLCs) (Box 1.3).

Box 1.3: SOE Restructuring – A Case Study of Malaysia

Malaysia’s experience in restructuring and managing SOEs, or government-linked companies (GLCs) in Malaysian nomenclature, provides interesting insights inthe use of key performance indicators (KPIs), linking the performance of SOEs to remuneration of management.

In 2004, the Government of Malaysia embarked on the Transformation Program, a comprehensive reform program of GLCs. The government aimed to improve the performance of GLCs and convert them into profitable, financially self-sufficient enterprises. The program adopted realistic objectives in line with international best practice.

Overall, five key factors contributed to the success of GLC transformation:

- the establishment of a government body with a clear mandate and objectives in relation to enhancing the performance of GLCs;

- development and monitoring of KPIs;

- sound accountability framework for delivering results;

- strong focus on profitability; and

- appointment of qualified professionals.

A central body in the Transformation Program was the Putrajaya Committee on GLC High Performance chaired by the deputy finance minister and comprising representatives of all key SOE shareholders and experts. Shortly after its establishment in 2005, the committee produced in 2006 a guidebook, Blue Book: Guidelines on Announcement of Headlines KPIs and Economic Profit (OECD 2016). The book established KPIs to be reported by GLCs in a consistent manner, aligning expectations at all levels.

The book tasked every GLC to annually file KPIs concerning its financial, nonfinancial, organizational, and operational goals, which were audited and benchmarked with comparable international peers. Based on the audit, the committee analyzed causes of underperformance and was able to mitigate weaknesses in a timely and targeted manner.

In addition to KPIs, the committee introduced performance-based contracts and compensation schemes, along with a change in the composition of GLC board members and senior management. The Malaysian government upgraded the legal and operational framework of the GLCs to corporatize them and infused into GLCs newer management practices from the private and public sectors.

The new management received a clear mandate along with indicators to improve SOE performance. Performance-based contracts linked GLC performance to the remuneration of GLC management, which meant that management had similar incentives as those in the private sector.

These reforms helped instill a performance-based culture and improved GLC management, which subsequently translated into higher GLC profitability— between 2004 and 2014, 20 of Malaysia’s largest GLCs operating overseas tripled their market capitalization.

Source: Authors, based on OECD (2016)

One way to improve oversight is to introduce a central SOE organization, while reforms are introduced to sector ministries. To minimize the ad hoc ministerial interventions in SOE matters, some developing countries have introduced a central oversight or coordinating organization. This central body typically reports only to the President or Prime Minister, the cabinet, or a special interministerial group. By breaking the one-on-one relationship between the sector ministries and the managing director, the central coordinating organization introduces a check and balance against political intervention.

Despite rather mixed reviews of its track record, such an organization can be beneficial to improving the coordination between different stakeholders. Lessons from the experience of different countries suggest that the central oversight body would be more successful if it has a small and dedicated staff, the full support and backing of the competent authority, and a clear mandate to deal with relevant ministries.

To maintain a balance between autonomy and accountability, governments in some developing countries have established holding companies by creating conglomerates, thereby increasing the size and power of SOEs vis-à-vis ministries—this can work in favor of autonomy. However, there are certain pros and cons for such an arrangement. For example, by exploiting economies of scale, these holding companies can work more efficiently in the international capital and export markets than smaller companies. In such a setup, it is relatively easier to liquidate a nonviable subsidiary than a freestanding SOE; at the same time, these holdings also provide an effective buffer against political interference.

On the negative side, large holdings comprising mainly unrelated subsidiaries often tend to become very political and bureaucratic in nature. If there is still political interference, these huge conglomerates may promote monopolistic or oligopolistic behavior. Under such circumstances, instead of closing nonviable operations, these holdings may shift funds, inventories, and skilled staff from profitable units to nonperforming units, keeping alive nonviable firms and thus

dragging down the performance of the holdings (Shirley 1989).

1.11 Relevance of SOEs in Asia’s Next Transition

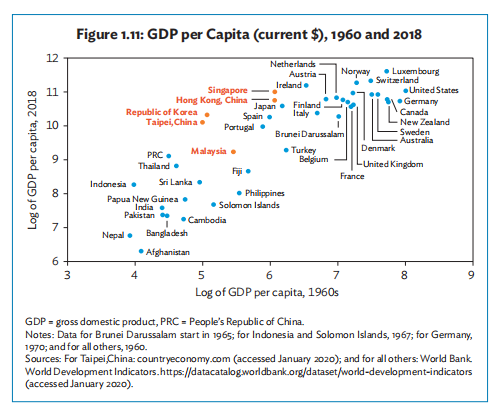

Developing Asia’s economy has grown robustly at 6.9% per annum during 1970–2019. A comparison of per capita incomes across the region suggests that in the early 1960s, a majority of the population was living in low-income economies; however, by 2018, most of them lived in middle-income countries.

This experience has motivated policy makers and governments to prepare for Asia’s transition to high-income status. Can Asia’s success guarantee a similar transition from middle income to high income and can the improved performance of SOEs facilitate the transition?

Experience across economies has revealed the structural difference of middle-income and low-income economies, and that graduation from middle income to high income can be quite challenging. An examination of the Asian economies that have transitioned successfully to high-income status suggests that improvement in productivity played an important role in their transition and in sustaining high growth over a longer period. For example, in Asia, Singapore; Hong Kong, China; the Republic of Korea; Taipei,China; and Malaysia are the only economies that have transitioned to high-income status (Figure 1.11).

Empirical evidence reveals that to meet the challenges of middle-income transition, countries need more cutting-edge technologies and frontier innovation to sustain knowledge diffusion as their income levels rise. This would require greater investments in human capital and research and development (R&D) thereby allowing countries to adopt globally existing technologies.

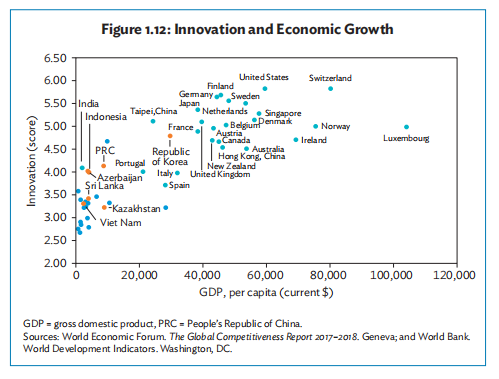

Another priority would be to ensure that the relatively more productive enterprises in an economy are able to engage in and reap the benefits of the latest innovations. In Figure 1.12, the comparison of per capita income and the innovation score reveals that economies already in advanced stages of development tend to score better on innovation. On the other hand, lower-income and middle income economies also score lower on innovation. This suggests that economies that have adopted policies promoting competition and a level playing field perform better in producing quality products.

The capability to innovate and to bring innovation successfully to the market is crucial in improving the global competitiveness of DMCs. However, it is equally possible for economic growth and other macro factors to affect innovation activities, implying that in practice both innovation activities and economic growth can bring about the other, and therefore there is a potential for feedback relationship between the two (Maradana et al. 2017).

To promote innovation-led growth, DMCs should ensure the growth of innovative enterprises to an efficient scale and also encourage the entry of new firms while discouraging the survival of less-productive entrepreneurs. The political economy and the quality of existing institutions will likewise play a more prominent role as a country approaches the technology frontier (Aghion and Bircan 2017).

The prevalence of SOEs and state ownership in developing countries suggests that governments should promote policies that create a level playing field and a sense of dynamism in public companies to foster innovation. This will require a balance between the SOEs’ objectives and the services that private entrepreneurs are better able to produce. The idea is that policy objectives and instruments should be tailored to a country’s level of development and the strengths and weaknesses of its innovation system. More importantly, governments need to increase R&D expenditure to promote a culture of innovation. DMCs can enhance such a transition through reforming SOEs and making them an efficient driver of growth.

An examination of economies that have transitioned successfully from low[1]income to high-income status reveals that the role and nature of the public sector changes in parallel with the stages of development. For example, at early development stages when the private sector is not yet fully developed, the public sector can play a significant role in promoting economic development.

During this stage, governments often have relatively better human capital, and public policies and programs mainly focus on identifying key development bottlenecks and coordinating capacity-building efforts in infrastructure and human capital. With weak private financial institutions, it is also challenging to secure financing for large-scale projects, and private investors remain reluctant. In such cases, government financing and SOEs could take the lead in providing the necessary infrastructure for economic development. The Republic of Korea’s experience emphasizes the importance of the changing role of the public sector in different stages of development (Box 1.4).